There is a firm that has done everything H2 described.

It crossed the Trust Ceiling. It built genuine growth leverage — reach into a market the customer could not access alone, an ecosystem relationship that opened doors, a perspective the customer’s leadership now seeks before a strategy is finalised, not after. The firm has a seat at the table. It is in the room while the thinking is still forming. By the standard the previous article set, this firm has arrived.

And yet, when the conversation turns to economics — to revenue share, to co-investment, to a genuine stake in what is being built — the answer is polite, warm, and unmistakably no.

The firm is not being dismissed. It is being thanked. Its perspective is valued. Its presence in the room is welcomed. But the room’s output — the value created by the strategy the firm helped shape — remains entirely the customer’s. The firm shaped the direction and was paid its fees for doing so. Nothing more was offered, and nothing more arrives.

This is not the Trust Ceiling. The firm crossed that. This is a different ceiling, one storey higher, and it catches firms precisely because they believed crossing the first one was the hard part.

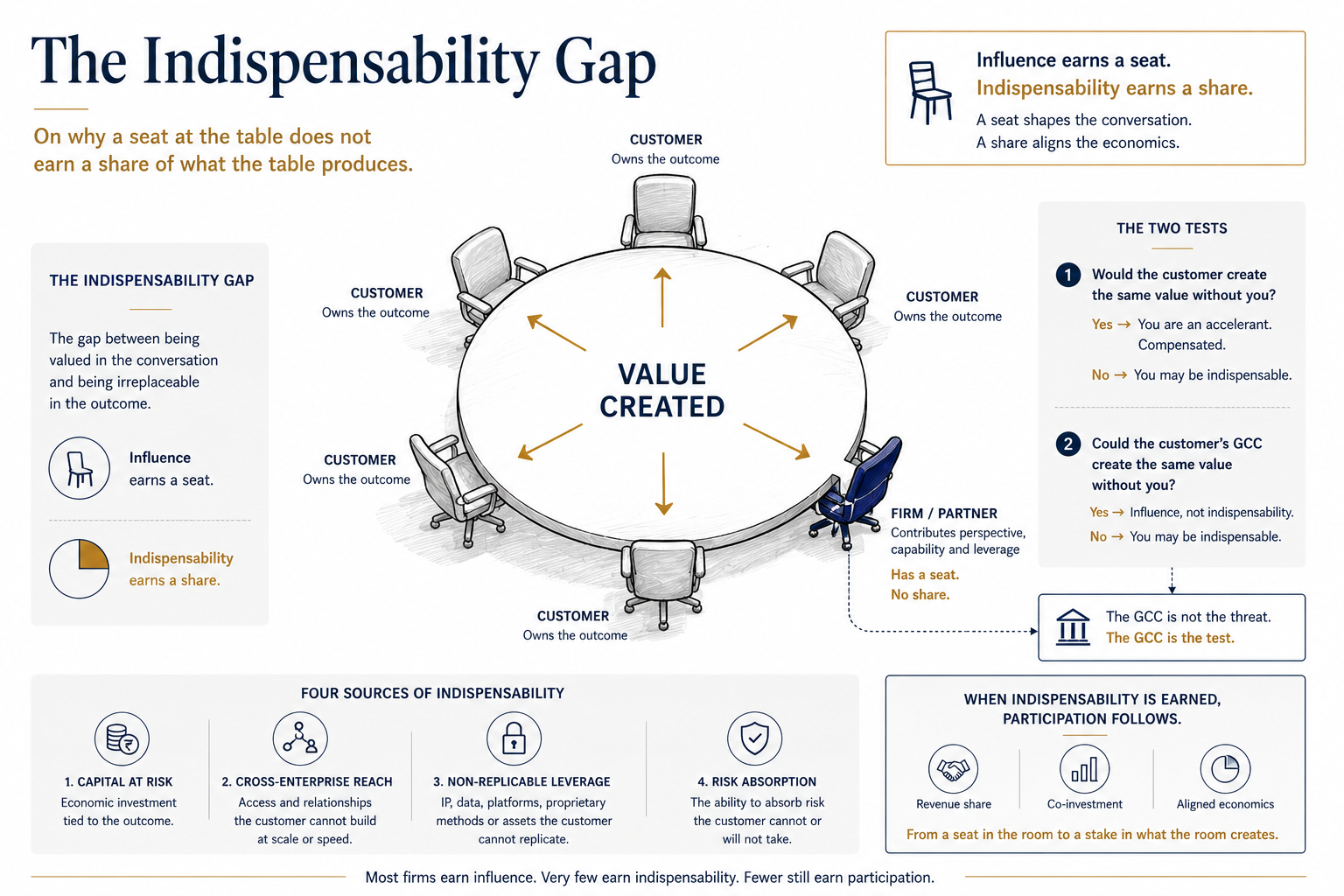

Influence Is Not Indispensability

A seat at the table answers one question: can this firm contribute to how we think?

A share of what the table produces answers a different question entirely: would this outcome exist without this firm?

These are not the same question, and the gap between them is where most firms that have successfully built influence quietly stall. Influence is about access to the conversation. It is earned by being useful to have in the room — informed, connected, capable of seeing around corners the customer cannot see around alone. A firm can have real influence, exercised consistently and valued genuinely, and still be one of several voices the customer could substitute without the outcome changing.

Indispensability is about what happens if the firm leaves the room. Not what is lost in comfort, or relationship, or familiarity — what is lost in the outcome itself. If the firm’s chair were empty, would the strategy still arrive at the same place, by a different route, perhaps more slowly, but the same place? Or would the destination itself be different — a market not entered, a capability not built, a future the customer would not have reached on their own?

Influence is earned through relationship and perspective. Indispensability is earned through something the customer cannot replicate — not easily, not quickly, and critically, not internally either. This is the gap the title names. The Indispensability Gap is the distance between being valued in the conversation and being irreplaceable in the outcome. Most firms that have crossed the Trust Ceiling have not yet crossed this one, and very few notice the difference until they ask for participation and receive, instead, gratitude.

The practical consequence of this gap is participation — or the absence of it. Influence earns a seat. Indispensability earns a share. A seat shapes the conversation. A share aligns the economics. The first is granted relatively freely, because it costs the customer little — a chair, a calendar slot, a willingness to listen. The second is granted rarely, because it costs the customer something real: a portion of the value itself. Most firms spend years working to deserve the first and are surprised when it does not, on its own, unlock the second.

The Test

There is one question that cuts through every justification a firm offers for why it deserves a share of the value it helped create.

Would the customer create the same value without you?

This is not a question about whether the firm is good. Good firms ask it and discover the honest answer is yes — the customer would likely arrive at a similar outcome, perhaps less elegantly, perhaps on a longer timeline, but the value would still exist. If the answer is yes, the firm’s contribution — however excellent — was an accelerant, not a source.

Accelerants are compensated. They are not made partners in what they accelerated.

If the answer is no — if the market would not have been entered, the capability would not exist, the relationship would not have been built — something has changed. The firm is not merely present in the value creation. It is a condition of it. That is the threshold indispensability requires, and it is a far higher bar than influence ever was.

But there is a second version of this question that technology services firms increasingly cannot avoid, and it is the one that makes this article different from a generic indispensability argument.

Could the customer’s GCC create the same value without you?

For two decades, the comparison that mattered was the firm versus the customer’s own internal team — usually thin, usually focused on operations, rarely a serious alternative for anything strategic. That comparison is no longer the relevant one. Global Capability Centres have matured. They are not back-office cost centres anymore. Many run platforms, own roadmaps, employ senior technical and strategic talent, and are explicitly mandated to build capability that previously sat with external partners.

A firm that passes the first test — the customer alone could not do this — can still fail the second. The customer’s GCC, given the mandate and the time, could.

Why The Second Test Matters More Than The First

Most technology services leaders, when they think about defending their position, think about GenAI. Fewer think carefully about GCCs, and fewer still connect the two.

But here is the structural reality. GenAI compresses the value of execution — it makes the things a firm used to be paid to do cheaper and faster to do, for everyone, including the customer. GCCs internalise execution — they bring the things a firm used to be paid to do inside the enterprise, staffed by people who report to the customer, not to the firm.

These are different mechanisms. But they converge on the same question, and a firm that has built influence without indispensability is exposed to both simultaneously. GenAI says: the execution this firm provides is becoming less scarce everywhere. The GCC says: and even where it remains valuable, we are increasingly equipped to provide it ourselves.

A firm that has only built influence — a seat at the table, a trusted perspective — has nothing in its position that either force respects. GenAI does not care that the firm is trusted. The GCC does not care that the firm has a good relationship with the CTO. Both forces are, in their own way, asking the same blunt question the indispensability test asks: if this firm were not here, what would actually be missing?

For most firms, today, the honest answer is: less than they think. Not nothing — relationships have value, perspective has value, continuity has value. But not enough to be irreplaceable, and “not enough to be irreplaceable” is precisely the position that earns gratitude rather than participation.

What Indispensability Actually Requires

Indispensability is not claimed. It is demonstrated, and it is demonstrated through one of a small number of things that neither GenAI nor a GCC can replicate by design, not merely by current limitation.

Capital at risk. A firm that has put its own money behind an outcome — co-invested in a venture, taken a position in the result rather than a fee for the work — has changed what it is. It is no longer a vendor whose risk ends when the invoice is paid. A GCC, funded entirely by its parent’s budget, structurally cannot take this position. It has no balance sheet of its own to risk.

Reach across enterprises. A firm that has built relationships, market access, or ecosystem positions across multiple clients carries something no single customer’s GCC can replicate, because a GCC exists to serve one enterprise. This is the heart of the structural law: a GCC is designed to optimise one enterprise. The Expansion Zone is built on leverage across enterprises. Cross-client pattern recognition — knowing what worked in three other transformations because the firm was present for all three — is not a capability gap a GCC can close by hiring more people. It is a structural feature of being embedded in one organisation rather than many.

Leverage that cannot be replicated. Proprietary platforms, intellectual property, or capabilities built over years across multiple engagements. Not a process document. Something genuinely difficult to recreate from scratch, internally, on any reasonable timeline.

Risk absorption. A willingness to carry downside — financial, operational, or reputational — that the customer prefers not to carry themselves. This is different from capital at risk; it is about absorbing consequence, not just investment. A firm that says “if this fails, the cost falls on us, not only on you” has changed the nature of what it is offering.

None of these are claims a proposal can make convincingly. They are positions a firm either occupies or does not, and the occupying takes years, not a pitch deck.

The GCC Becomes The Test, Not The Threat

Here is where the argument inverts, and where it becomes genuinely useful rather than merely diagnostic.

A firm that cannot pass the GCC test — whose value the customer’s internal capability could replicate given time and mandate — has correctly identified its exposure. But a firm that can pass the GCC test has found something more valuable than a defence. It has found a description of what it actually is.

Because the things that pass the GCC test — cross-enterprise reach, capital at risk, leverage built across many engagements, risk genuinely absorbed — are not things a GCC competes for. They are things a GCC, by its nature, needs. A mature GCC that has internalised execution still cannot give its parent organisation access to patterns from outside the enterprise, cannot co-invest in a venture using its own capital, cannot bring an ecosystem relationship that exists because of work done elsewhere.

The GCC, in this light, stops being the threat the firm is positioned against. It becomes evidence of where the firm’s value genuinely sits — and, increasingly, a customer for that value in its own right. A firm with real cross-enterprise leverage does not compete with a customer’s GCC. It is one of the few things a GCC cannot become on its own, and one of the few things a sophisticated GCC will actively seek out.

Participation Follows. It Is Not Pursued.

The natural instinct, on reading this, is to ask how a firm gets participation — how to structure the ask, how to position the proposal, how to make the case.

That instinct is itself part of the problem. Participation is not negotiated into existence by a firm that has not yet earned indispensability. It is recognised, often without much negotiation at all, once indispensability is established — because at that point the customer’s own question changes. It stops being “why should we give this firm more?” and becomes “what happens to this relationship if this firm’s interests and ours are not aligned?”

That question, asked honestly by a customer, is the moment participation becomes available. Not as a reward for past contribution, but as the only structure that makes sense once the customer recognises that the firm’s continued presence is a condition of the value they are now relying on.

The work, then, is not to ask for participation. It is to become the kind of firm for which the question of participation answers itself — across enterprises, with capital and risk genuinely at stake, in ways that neither a faster model nor a better-resourced internal team can replicate.

Run This In Your Organisation

Five questions for leadership teams asking why influence has not become participation.

Question 1 — The empty chair test

Take your most influential customer relationship — the one where you are most genuinely “in the room.”

If your firm’s chair were empty for the next strategic planning cycle, what would actually be different in the outcome? Not the process. The outcome.

Write the honest answer in two sentences. If the answer describes a slower or less comfortable path to the same destination, you have influence without indispensability.

Question 2 — The GCC test

For that same relationship — does the customer have a GCC, or a capability internally that is growing toward what you provide?

If given an eighteen-month mandate and the budget your engagement currently represents, could that internal capability deliver what you deliver?

Be specific about what would be hardest for them to replicate — and whether that hard part is actually what you currently get paid for, or something else you have not yet made visible.

Question 3 — The cross-enterprise audit

Name one thing you know, have access to, or can do — for this customer — specifically because of work you have done with other clients, in other markets, or across your wider business.

Not a process template. Something genuinely born of being in many places at once.

If you cannot name something specific, your cross-enterprise leverage is not yet visible to the customer — which means, for their purposes, it does not yet exist.

Question 4 — The risk position

In this relationship, what happens to your firm if the outcome fails?

Does the engagement simply end — invoices stop, the team moves on — or does your firm carry a cost: capital invested, revenue tied to the outcome, reputation genuinely staked?

Name the actual consequence to your firm of failure. If there isn’t one beyond the loss of future work, you are not yet carrying risk in a way the customer can feel.

Question 5 — The first move

Of the four sources of indispensability — capital at risk, cross-enterprise reach, leverage that cannot be replicated, risk absorption — which one is closest to true for this relationship today, even if not yet structured or visible?

What would it take to make it real, and then visible?

Who owns starting that conversation — not the ask for participation, but the work that would make the question of participation answer itself?

By when?

Influence earns a seat at the table. Indispensability earns a share of what the table produces. The distance between them is not closed by asking for more. It is closed by becoming something a GCC cannot become and a faster model cannot replace — present in enterprises plural, not singular, with something genuinely at stake.