There is a question that has started appearing in client conversations that did not appear five years ago.

Not in the format reviews. Not in the delivery assessments. In the conversations that happen after the metrics are shared — when the room settles into something less structured and someone, usually the most senior person on the client side, asks something that does not fit the quarterly template.

The question sounds simple. It is not.

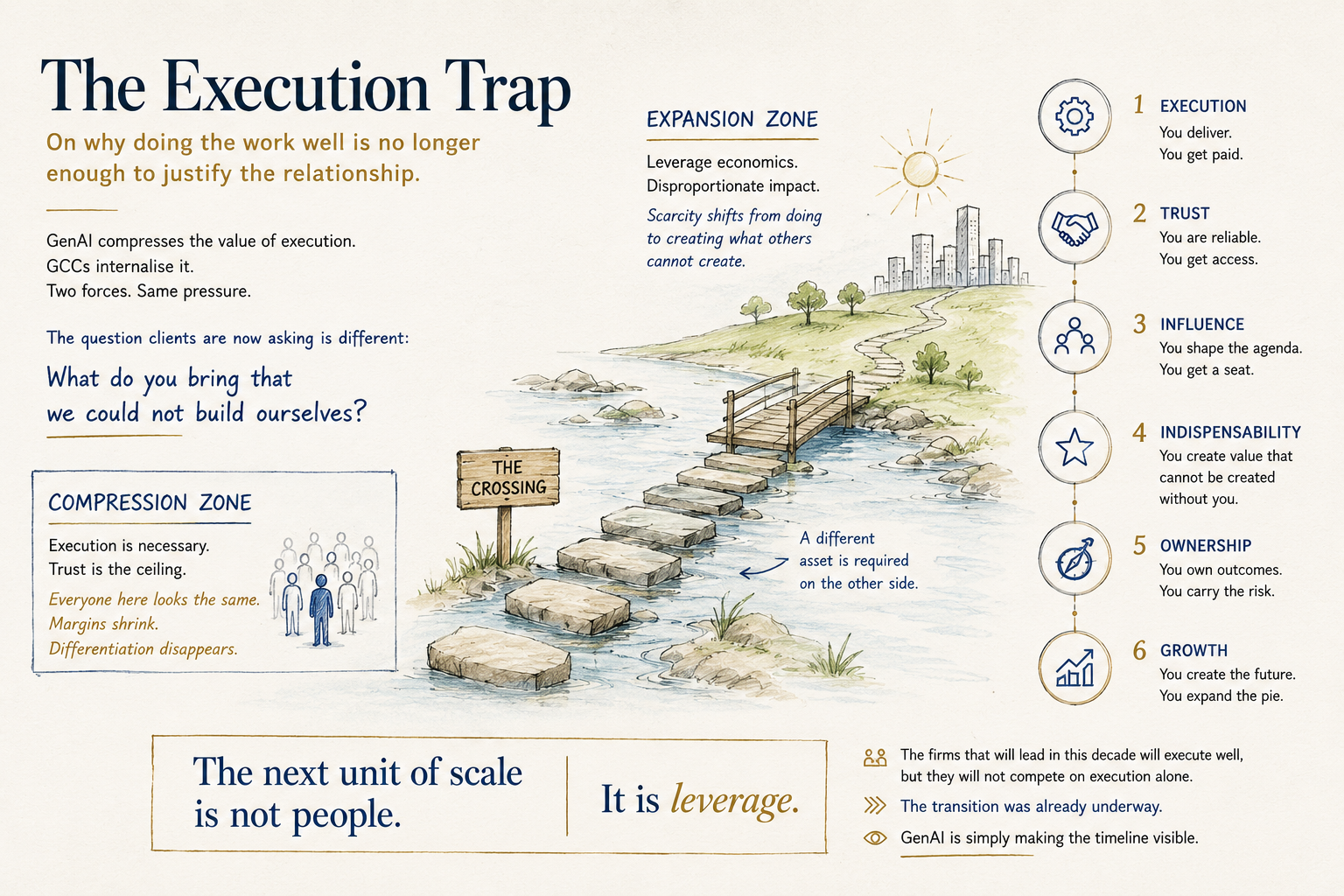

What do you bring that we could not build ourselves?

Not: can you deliver this. That question was answered years ago. Not: can we trust you. That question was answered too. What the client is asking — and in some rooms is beginning to ask out loud — is whether the relationship has a future that justifies its current shape. Whether what the partner brings is something the client genuinely cannot replace. Whether there is a reason, beyond inertia and switching cost, to keep the relationship structured the way it is.

That question marks a boundary. Before it, execution was enough. After it, something else is required.

The Historical Unit of Scale

For three decades, the answer to that question was simple enough that most leadership teams never had to ask it explicitly.

More demand required more people. More people produced more delivery. More delivery generated more revenue. The unit of scale in technology services was human capability — the ability to recruit, develop, and deploy qualified talent at volume and at pace. Firms that mastered this unit grew. Every new wave of customer demand created a new wave of hiring. Growth was legible, measurable, and largely predictable.

The equation was already weakening before GenAI arrived. GenAI did not create the breakdown. It made the breakdown impossible to ignore. The relationship between demand and people has changed: a firm that once needed fifty engineers to deliver a capability may now need fifteen. The historical unit of scale has broken down.

The question that should be sitting at the centre of every technology services leadership conversation is not how to execute better. It is: what becomes the next unit of scale?

The Transition That Was Already Underway

Answering that question requires seeing the pattern that preceded it — specifically, what customers were buying in each era, not what firms were selling.

In the 1990s, customers were buying scale. The ability to build large systems, field large teams, and deliver at a volume their own organisations could not match. Scale was genuinely scarce, and the firms that could provide it built durable competitive positions on that scarcity.

In the 2000s, customers were buying reliability. The infrastructure had been built. Now it needed to run — consistently, at quality, across increasingly complex environments. Customers were no longer buying talent alone. They were buying predictability. Operational discipline became the scarce asset, and managed services emerged as the commercial model that delivered it.

In the 2010s, customers were buying transformation. Cloud migration, digital reinvention, agile ways of working, automation — customers needed to change how they operated, not just optimise what they had. The firms that could navigate large-scale change while keeping existing operations stable earned significant premiums. The language of the era spoke of platforms and outcomes, though the economics remained largely execution-driven.

In the 2020s, customers are buying leverage. They have infrastructure. They have operations. They have, largely, digital foundations. What they now need is the capacity to move faster, expand further, and create value they could not create with what they already have. Execution does not provide leverage. Scale, reliability, and transformation capability, while necessary, do not answer the leverage question.

This is the pattern GenAI is accelerating — not creating. Each wave commoditised what the previous wave had made scarce. Each wave required a new answer to the question of what the firm was actually worth. GenAI is compressing the value of execution faster than any previous wave compressed its predecessor. Execution still matters. It simply no longer differentiates at the level it once did.

The Compression Zone

GenAI is not eliminating execution. It is compressing the economic value of execution. And that compression is the defining strategic reality of technology services in this decade.

The execution layer is entering a Compression Zone. Not because the work is disappearing, but because the basis of competition within that layer is converging. Faster. Cheaper. More reliable. These are not positions — they are the minimum requirements for being in the conversation. A firm that competes on execution quality alone is competing in a space that is simultaneously growing in volume and shrinking in margin. Every improvement it makes is matched by the next firm that acquires the same capability.

The danger is not poor execution. The danger is becoming world-class at something customers increasingly view as a baseline expectation.

But GenAI is not the only force. Global Capability Centres are growing across every major customer segment — and they are asking a different question. Not: can a machine do this faster? But: why do we need an external provider to do this at all? GCCs are built to internalise execution — to bring talent, operations, and delivery inside the enterprise. GenAI compresses the value of execution. GCCs internalise it. One reduces what execution is worth. The other eliminates the need for a partner to provide it. Two forces, different mechanisms, same pressure. And the same question underneath both: what remains valuable when execution is no longer what you are selling?

The challenge is not how to survive compression. The challenge is how to earn entry into the Expansion Zone — the terrain where influence, indispensability, ownership, and growth operate on fundamentally different economics. That challenge has a six-step answer.

The Six Steps

Most firms do not fail at this transition because they lack capability. They fail because they are trying to earn a reward that belongs to a higher stage using assets designed for a lower one. Execution earns trust. But once trust is earned, executing harder does not earn access — a different credential is required. Trust earns access. But once access is earned, demonstrating trustworthiness more emphatically does not earn a seat — influence is required, not reliability. Each rung unlocks the next. But more of the same rung never does. The firm that recognises itself in this — capable, trusted, present, and still excluded from the conversations that matter — is the firm this series is written for.

Execution earns compensation. It is the entry ticket — the minimum required to be in the conversation. Without it, nothing else is possible. But execution, however excellent, is not the credential that unlocks the next rung. Executing better earns more compensation. It does not earn access. That requires something execution alone cannot produce.

Trust earns access. A customer who trusts a partner invites them into more rooms, more conversations, more planning cycles. Trust is built through consistent delivery — through showing up under pressure, honouring commitments, and being depended upon. These are genuine achievements. But trust is the highest reward available inside the Compression Zone — and the only one. The industry’s most dangerous misconception is that trust is the destination. It is not. Trust is the reward for execution. Influence is the reward for leverage. Trust, however deep and however earned, is the ceiling of what the Compression Zone can provide. The firms that make the crossing use trust not as a destination but as the credential that unlocks the door to influence. Most firms never make that crossing. Not because they lack trust. Because they do not recognise that a different asset is required on the other side.

Most firms never realise they are trapped. The customer trusts them. Revenue grows. Renewals continue. The relationship appears healthy. Yet every strategic conversation happens somewhere else. Trust has been earned. Influence has not. That gap — invisible from the inside, visible from the outside — is where most technology services relationships quietly stop evolving.

The boundary between the two zones has a name: The Crossing.

Influence earns a seat. Influence begins before the buying process begins. When the client decides where to place its next significant technology investment, influence determines who is invited before the RFP exists — and whose perspective shapes the decision once the conversation begins. Influence is not earned by executing more reliably. It is earned through growth leverage — the demonstrated capacity to help the client see possibilities they had not identified, reach markets they had not considered, or move faster than their own resources would permit. In practice, this means the partner introduces a market opportunity, a strategic ecosystem relationship, or a faster path to growth that the client would not have identified independently. A seat at the table, however, is not the same as a share of what the table produces. Access brought you into the room. Influence gives you a place to sit. Indispensability determines whether you share in it.

Indispensability earns participation. A firm that has become indispensable does not bill for hours. The discussion moves from rates and utilisation to participation and upside. But indispensability is not claimed — it is demonstrated. It requires something the client cannot build alone: capital at risk, reach into new markets, leverage that cannot be replicated, or risk absorption that the client prefers not to carry. These qualities cannot be asserted in a proposal — only established by evidence. The test is simple, and it is the right one: would the customer create the same value without you? If the answer is yes, indispensability has not yet been established. If no — if markets, customers, or capabilities exist because of the partner that would not otherwise exist — participation follows as a natural consequence of the economics. But participation is an economic right, not a governance one. A share of the upside does not automatically produce the authority to make decisions. That requires something participation cannot provide.

Ownership earns control. Ownership is not the reward for proving readiness. It is the consequence of being the only one willing to carry what the outcome requires. The client stops measuring activity and starts measuring outcomes. The firm carries accountability for the result, not just the deliverable. Ownership is the most contested step in the progression because it requires the client to cede decision rights, not just economic participation. A client can share economics generously — gain-share, outcome-based structures, revenue alignment — and still withhold control, because the question they are asking about control is different from the question participation answered. Not: does this firm create value? But: will this firm carry the weight when the outcome fails? Control arrives when the answer to that second question is demonstrated, not claimed.

Growth earns the premium. Growth is not measured in what the firm delivers. It is measured in what becomes possible because the firm is there. When a firm helps a customer expand into new markets, new ecosystems, and new futures, it is no longer rewarded for what it does. It is rewarded for what it makes possible. The firm’s structure becomes an asset rather than a constraint. This is the destination the progression was always pointing toward — not ownership alone, but the premium economics that accrue to a firm built to move a customer’s trajectory, not just support its operations. And it is the answer to the question this article began with. The firm is no longer multiplying people to meet demand. It is multiplying opportunities. That is the next unit of scale.

A firm that attempts ownership before establishing indispensability will find the client unprepared to grant it. A firm that claims indispensability before building influence will find the claim unanchored. The sequence has its own logic, and it runs in one direction. Each rung is a different answer to the question this article opened with: what becomes the next unit of scale?

The series that follows maps this journey one step at a time — naming, in each article, the obstacle that stops most firms, the mechanism behind it, and the move that unlocks the next rung. But the map is here. The reader who reaches the final article will recognise that the whole journey was visible from this point.

Run This In Your Organisation

Five questions. For leadership teams of technology services firms asking where they stand.

Question 1 — The client question audit

In your three most important client relationships — what question is each client currently asking?

Is it a delivery question: can you do this reliably? Is it a growth question: can you help us create something we cannot create alone? Is it an indispensability question: why should we share the upside with you? Is it an ownership question: can we give you control of this?

Name the question that is actually active — not the one your last QBR was designed to answer. If you are not certain, ask the most senior person on the client side. The question they are asking determines the terrain you are competing on.

Question 2 — The differentiation test

If your three most important clients were asked — honestly — what they would lose if they replaced you with a credible alternative:

What would they say?

Is the answer execution quality and switching cost? Or is it something above that — influence in conversations, participation in outcomes, ownership of something that matters?

The honest answer tells you whether your firm is competing in the Compression Zone or building toward the Expansion Zone.

Question 3 — The GenAI exposure check

Name the three components of your current value proposition that are most directly affected by GenAI.

For each one — is the compression happening already, or is it still coming?

Now name what remains after those three components are compressed. That remainder is your Expansion Zone territory. If you cannot name it specifically, you have not yet found it.

Question 4 — The revenue defence question

What percentage of your significant client revenue is defended by something other than execution quality and switching cost?

Not aspired to be defended by something else. Actually defended — by influence, by indispensability, by ownership, by something the client would lose if you were replaced.

Write the percentage. If it is below twenty percent, the firm is still competing primarily in the Compression Zone. If it is below ten percent, the urgency is immediate.

Question 5 — The next step

Beyond execution, which of the remaining five steps is your firm currently on in your most important client relationship?

Trust. Influence. Indispensability. Ownership. Growth.

Which step is next? What does making that step require — in the commercial structure, in the operating model, in the conversation with the client?

Who in your organisation owns making it?

By when?

The firms that will lead technology services in the next decade will execute well, but they will not compete on execution alone. The transition was already underway. GenAI is simply making the timeline visible.